Why PAYE Calculation Changed in Nigeria

The Nigeria Tax Act 2025 replaced the older PITA framework and introduced revised income brackets, updated relief structures, and clarified the order in which deductions must be applied before tax is calculated. If your business is still using the old PITA brackets, every payslip since January 2025 has been computed on outdated figures.

Step 1: Calculate Annual Gross Income

Start with the employee's total annual compensation before any deductions — basic salary plus all taxable allowances: housing, transport, medical, and any other recurring payments.

Example: An employee earns ₦180,000 per month in basic salary plus a ₦40,000 housing allowance. Annual gross = (180,000 + 40,000) x 12 = ₦2,640,000.

Step 2: Apply Statutory Deductions Before PAYE

This is where most businesses get it wrong. Pension, NHF, and NHIS must be deducted from gross income before PAYE is applied. These are pre-tax deductions. The order is mandatory under NTA 2025.

Pension: Employee contributes 8% of pensionable income (basic + housing allowance).

NHF: 2.5% of basic salary monthly, formal sector only.

NHIS: Typically 1.75% of basic salary (scheme-dependent).

Using the example: Annual pension = ₦211,200. Annual NHF = ₦54,000. Annual NHIS = ₦37,800. Total pre-tax deductions = ₦303,000.

Step 3: Apply Tax Reliefs

Consolidated Relief Allowance: ₦200,000 per year or 1% of gross (whichever is higher),

plus 20% of gross income.

Rent relief: 20% of annual rent paid, capped at ₦500,000 per year.

Life assurance premiums: Full premium deductible.

Mortgage interest: Interest on owner-occupied property mortgage is deductible.

Step 4: Calculate Taxable Income

Taxable income = Annual gross minus pre-tax deductions minus tax reliefs.

Example: ₦2,640,000 - ₦303,000 - ₦728,000 (consolidated relief) = ₦1,609,000 taxable income.

Step 5: Apply the NTA 2025 PAYE Brackets

₦0 — ₦800,000: 0%

₦800,001 — ₦2,800,000: 15%

₦2,800,001 — ₦8,000,000: 18%

₦8,000,001 — ₦18,000,000: 21%

₦18,000,001 — ₦32,000,000: 23%

Above ₦32,000,000: 25%

For ₦1,609,000 taxable income:

First ₦800,000 at 0% = ₦0

Remaining ₦809,000 at 15% = ₦121,350

Annual PAYE = ₦121,350 | Monthly = ₦10,113

Why Manual Calculation Is Risky

The multi-step nature of PAYE — pre-tax deductions, multiple relief types, progressive brackets — means a single formula error in a spreadsheet produces wrong results for every employee, every month. Payroll errors compound over time. FIRS does not distinguish between intentional underpayment and calculation errors. Both create a liability.

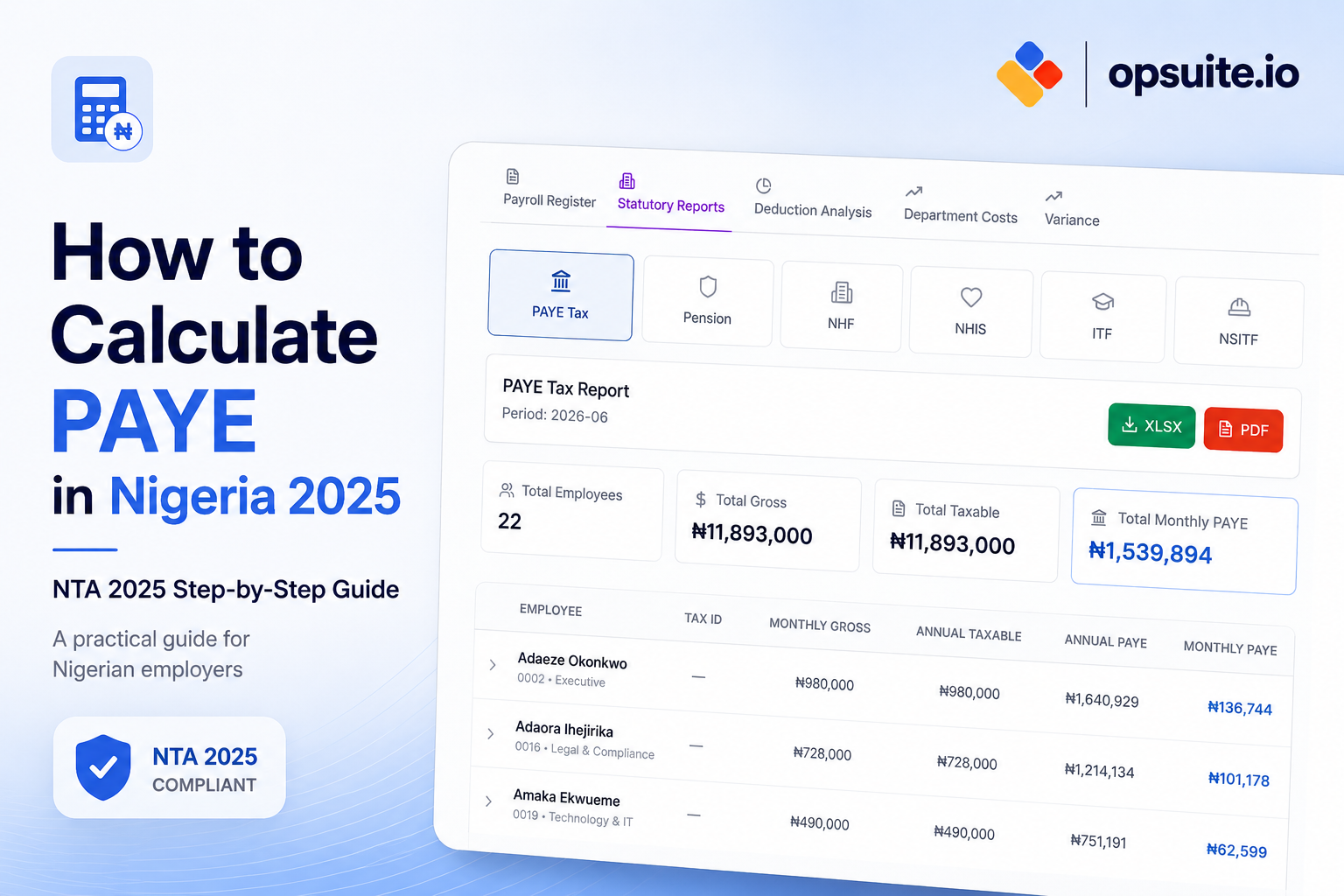

How Opsuite Automates This

Opsuite Payroll performs every step above automatically. NTA 2025 brackets are hardcoded. Deduction order is correct by design. Each staff member's reliefs are configured once and applied every cycle. You see a full transparent breakdown before confirming payroll.

Run a free simulation at opsuite.io/modules/payroll or start your 7-day free trial at app.opsuite.io.